Accounting for healthcare is a specialized branch with a focus on managing the financial complexities of dental and healthcare facilities. From transactions to regulatory compliance, it addresses the unique financial challenges of the medical industry.

Accounting for healthcare differs from standard accounting principles, as it requires special knowledge of different regulatory compliance, such as HIPAA, Medicare billing, and health insurance.

This specialized accounting branch ensures compliance, cost control, and financial transparency in different medical settings, including dental clinics, hospitals, and even private practices.

The responsibilities of accountants specializing in healthcare involve:

- Recording, interpreting, and managing financial records

- Analyzing cash flow statements

- Recording taxes and managing bills

- Preparing payroll for employees

- Collecting payments from patients

- Managing customer insurance claims

- Controlling equipment, staff, and medical supplies expenses

Accounting for healthcare helps medical facilities in providing better healthcare services to patients by taking care of financial matters. This way, healthcare providers can make better decisions, effectively manage their monetary affairs, and achieve sustainability in their practices.

Why Healthcare Needs Specialized Accounting?

Healthcare needs specialized accounting to cater the unique financial challenges and regulatory compliance. Unlike other sectors, dental and healthcare accounting requires management of a vast array of financial and regulatory affairs, including insurance claims, compliance reporting, operating costs, staff and supplies costs, third-party reimbursements, etc.

According to the Centers for Medicare & Medicaid Services (CMS), in 2022, the national health expenditure in the U.S. reached approximately $4.5 trillion, which is around 17.3% of the GDP. This corroborates the importance of effectively managing the healthcare expenses. Moreover, various financial aspects in the healthcare sector do not match standard business models, such as:

- Revenue cycles are based on reimbursements from insurers or government programs

- Compliance with HIPAA, HITECH, and IRS rules

- Inventory tracking of medical supplies and pharmaceuticals

- Value-based payment models, rather than fee-for-service only

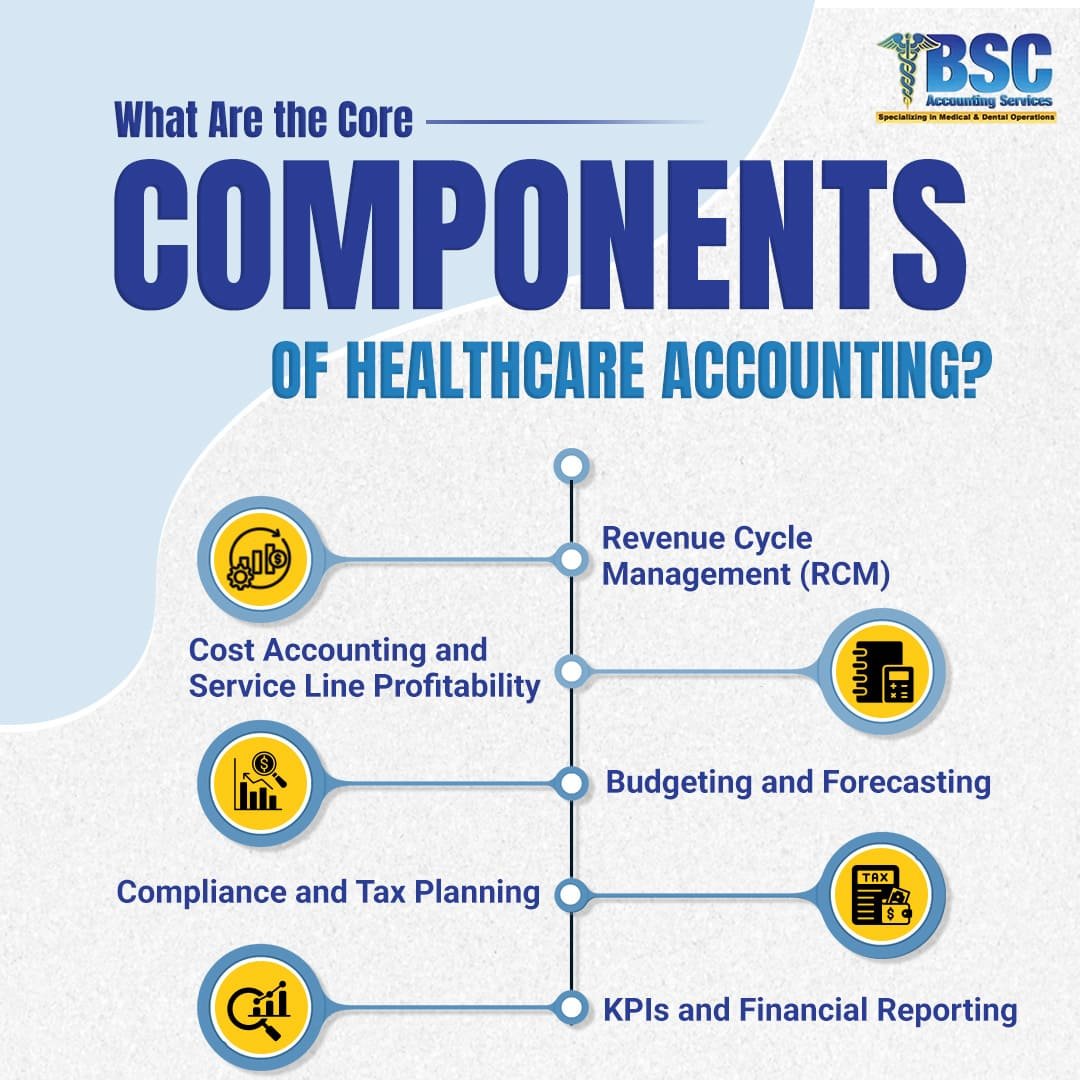

What Are the Core Components of Healthcare Accounting?

There are five core components, such as revenue cycle management and budgeting and forecasting, among others. These essential components ensure medical and dental facilities remain financially stable, compliant with regulations, and capable of making well-considered decisions.

1. Revenue Cycle Management (RCM)

RCM’s process entails tracking patient care from initial appointment to final payment. It includes scheduling, insurance verification, coding, billing, collections, and denial management. Studies show that efficient RCM reduces average days in A/R, improving cash flow, which is a critical success factor for the medical sector. If done right, it can improve the net revenue of healthcare organizations by 3-5% per year, which is proven by many industry analyses.

2. Cost Accounting and Service Line Profitability

Cost accounting in healthcare involves assigning direct and indirect costs to patient services. This helps in understanding profitability at the department or treatment level. For instance, dental practices track procedure costs (crowns vs. fillings) to guide pricing and investments.

In hospitals or large clinics, service line profitability analysis informs decisions about whether to expand or downsize specific departments based on their expense and usage.

3. Budgeting and Forecasting

There are times when hospitals have a change in general costs. That can be caused by a hike in seasonal patient volumes, payer mix changes, regulatory shifts, and inflation in medical supplies. This means predictive modeling must account for these factors. Thus, financial decisions in healthcare practices rely on zero-based or rolling forecasts.

4. Compliance and Tax Planning

The tax challenges in the healthcare sector are also unique. For instance:

- Non-profit hospitals must meet IRS 501(c)(3) requirements.

- Dental clinics often benefit from Section 179 deductions for equipment

- New clinics may qualify for Qualified Business Income (QBI) deductions under IRC 199A.

Most healthcare professionals, especially in private practices, do not know these nuances. Moreover, federal and state regulations change over time, which can be confusing. This makes implementation of proactive tax strategies essential.

5. KPIs and Financial Reporting

The standard income statement and balance sheet do not suffice for healthcare providers. Their KPIs need to be industry-specific, which are not met with standard protocols. Common financial metrics in the healthcare sector include:

- Gross collection rate

- Net collection ratio

- Days in A/R

- Cost per encounter

- Operating margin by service line

How Is Healthcare Accounting Different from Regular Business Accounting?

Healthcare accounting differs from regular business accounting in three major ways: how revenue is collected, how labor is classified, and how assets and compliance are managed. For instance, it involves tracking medical equipment costs, managing different types of workers like contractors and part-time staff, and following strict healthcare rules. These factors make healthcare accounting more complex and specialized than standard business accounting.

1. Third-Party Reimbursements & Claims Reconciliations

Unlike retail businesses with direct payments, the medical facilities often juggle reimbursements from insurers, Medicare/Medicaid, and patients. Moreover, reconciling claim payments and denials is very time-consuming. However, these nuances are critical to ensure accurate revenue recognition under GAAP and ASC 606 standards.

2. Capital Expenditure and Equipment Leasing

Talking specifically about dental practices, they frequently invest in high-value technologies, such as digital X-rays, CAD/CAM systems, or laser equipment. Hence, choosing between leasing, buying, or financing these essential equipments require clear financial modeling and depreciation tracking, especially under new lease accounting rules (ASC 842).

3. Payroll & Contractor Classifications

Due to the critical shortage of healthcare professionals, many medical facilities hire locum tenens physicians, hygienists, or part-time administrative staff to bridge the gap. Hence, correctly classifying W-2 vs. 1099 workers is not only a compliance issue but also affect payroll taxes, benefits, and overhead ratios.

Maintain Financial Stability with Accounting for Your Healthcare Practice

Accounting for healthcare clinic goes beyond standard practices. From managing insurance reimbursements and tracking equipment depreciation to handling contractor pay and staying compliant with changing tax laws, it requires industry-specific knowledge and precision.

Thus, as a healthcare provider, whether you run a solo dental clinic or a multi-location specialty practice, you need accounting expertise to stay financially healthy while focusing on patient care.

You can easily achieve this, by connecting with our accounting experts specialized in the dental and healthcare sector to efficiently handle your healthcare accounts so you can focus on what matters most – your patients.

FAQ about What Is Health Care Accounting

We have answered the most pressing questions that you might have related to the basics of health care accounting and what makes it different.

Do healthcare clinics need specialized accontants?

Healthcare clinics need specialized accountants because they deal with procedure-level costing, equipment depreciation, and insurance billing that general accountants may not understand.

Can general accountants handle healthcare practices?

General accountants can struggle with healthcare accounting because they often lack the knowledge to manage reimbursements, compliance, and industry-specific tax strategies accurately.